From geopolitical shock to a circular future for India’s packaging

The current geopolitical storm has amplified the business case for sustainable domestic resource management over foreign crude dependency

16 Apr 2026 | By Divya Subramaniam

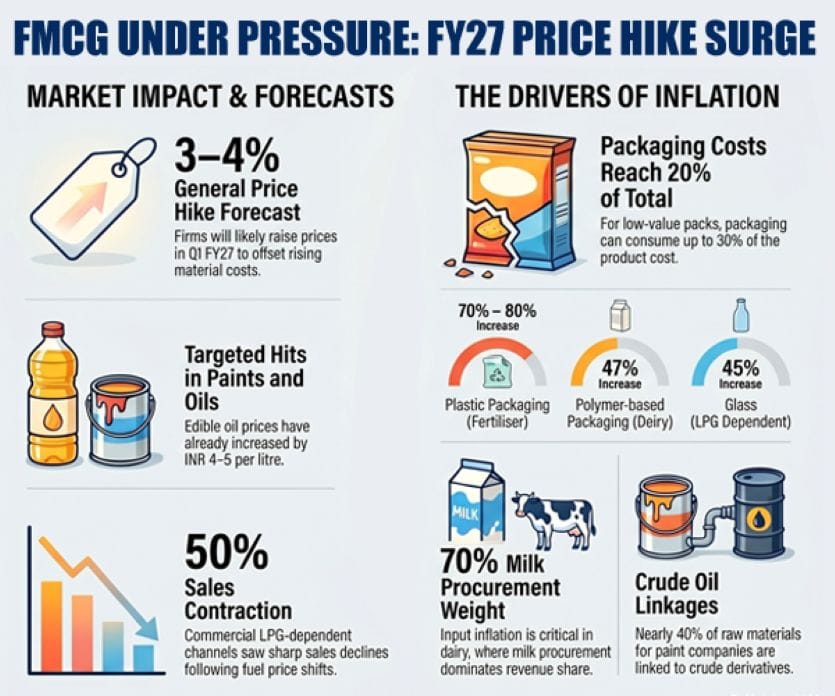

The FMCG price hike forecast, based on a report by Nuvama Institutional Equities, is for at least 3–4% in Q1 FY27. The price hikes could be even higher in some categories

The Indian packaging industry, the unseen engine of the nation’s supply chain, is currently enduring an intense geopolitical shock. For an industry that underpins everything from food security to consumer goods, the crisis radiating from the West Asia conflict — specifically, the blockade of the Strait of Hormuz — has exposed a critical vulnerability: an over-reliance on imported crude-oil derivatives. This is not just a temporary headache for business; it is a structural crisis forcing India to accelerate its long-overdue pivot towards a truly self-reliant, circular economy.

The immediate impact is a devastating surge in input costs, threatening to derail the nascent domestic demand recovery. Key petrochemical derivatives, such as polymers — which form the basis of most plastic packaging — have seen their prices spike by a staggering 50–60% in a matter of weeks. In the consumer packaged goods (FMCG) sector, where packaging accounts for 15–20% of total product cost, companies are bracing for price hikes of 3–4% in the June quarter (Q1 FY27), with even higher adjustments expected in categories like paints, edible oils, soaps, and detergents.

This inflationary pressure is forcing companies to employ recalibrated pricing strategies, including grammage reduction in smaller, price-sensitive packs, and outright price hikes in larger packs. The strain is evident across the economy. Dairy companies report polymer packaging costs soaring by about 47%, with glass packaging — dependent on commercial LPG for production — up around 45%. Supply bottlenecks have exacerbated the issue, packaging lead times have doubled, and many vendors are declining fresh orders.

Perhaps most critically, the crisis threatens India’s agricultural backbone. Fertiliser and seed companies are battling a packaging material crunch that could hinder deliveries during the crucial sowing season. The core issue remains plastics derived from crude oil, which is essential for preserving the viability of seed as a ‘living material’. With plastic packaging prices rising 70–80%, switching to alternatives is nearly impossible in the short term due to compatibility and redesign constraints. The crisis is most pronounced for low-value segments like bio-fertilisers, where packaging accounts for up to 10% of the end product cost.

Adding further pressure is the concurrent shortage of commercial Liquefied Petroleum Gas (LPG) — also a consequence of the West Asia conflict. This has impacted production in sectors like glass, textiles, and ceramics, forcing industrial units to operate at vastly reduced capacity (40–60%). In manufacturing hubs like Balasore, Odisha, plastic factories have seen production plummet by 70%, leading to machines falling silent and fears of mass contract job losses.

Government Intervention and De-risking

The Indian government has responded with targeted short-term relief measures. An official notification provided full Customs Duty exemption for about 40 critical petrochemical products, including polypropylene and polystyrene, until 30 June. This temporary relief is aimed at ensuring continued availability and easing cost pressure on downstream sectors.

Simultaneously, industry bodies have proactively consulted with the Commerce Ministry, requesting support to bolster corporate liquidity, particularly for Micro, Small, and Medium Enterprises (MSMEs). They requested the release of 20% higher working capital and a reduction of the Goods and Services Tax (GST) from 18% to 10% to bolster corporate liquidity, particularly for Micro, Small, and Medium Enterprises (MSMEs).

Beyond immediate firefighting, the crisis has spurred two crucial long-term strategies that represent India’s true resolution path.

First, the industry is strategically pivoting towards global exports. Recognising the volatility of relying on specific import regions, the plastics sector is leveraging recent Free Trade Agreements to actively explore 20 new markets, including Mexico, France, Brazil, and Japan. This move aims to grow India’s current meagre 1% share of the global finished plastic products trade, estimated at USD1.3 trillion. By diversifying its export base, India aims to build supply chain resilience and de-risk its plastic economy from regional geopolitical shocks.

The Circularity March

However, the definitive resolution to the packaging crisis lies in structural transformation: embracing the circular economy. The current geopolitical storm has only amplified the business case for sustainable domestic resource management over foreign crude dependency.

This shift is already gaining momentum. The global mandate to replace single-use plastic is fuelling a structural boom in the paper and corrugated packaging sector. Companies are focusing on energy efficiency and waste minimisation, moving towards a 'cost-minus' framework where profit is generated by eliminating internal inefficiencies. This focus is visible in the industry’s adoption of proprietary gas-combustion systems for manufacturing, reserving electricity solely for mechanical loads, and benchmarking energy performance.

For plastic, the path is clear. The industry experts who WhatPackaging? interviewed, talked about the "transition from virgin polymer to recycled and returnable solutions. Here, three trends emerge.

One is new developments, such as the Plastic Waste Management Amendment Rules 2026 and new solid waste management rules, signal a definitive policy shift towards circularity, providing the regulatory push the sector needs. Two packaging manufacturers are increasingly focusing on rPET (recycled PET) adoption, lightweighting, and tethered closures. Companies are investing in solutions like returnable packaging systems for the automotive and FMCG sectors, reducing material use and logistics costs. And finally, industry leaders are urging the government to work towards building a stable and integrated PVC value chain to insulate the domestic market from global geopolitical disruptions, ensuring long-term price stability for materials critical to agriculture and infrastructure.

India’s packaging crisis is a double-edged sword. While it delivers immediate pain through inflationary pressures and supply bottlenecks, it is also providing the fierce necessary impetus to break free from the constraints of a crude oil-dependent model. By combining strategic export diversification with a radical, policy-driven embrace of the circular economy, India is not just mitigating a crisis — it is forging a more robust, sustainable, and crisis-proof packaging ecosystem for the future. The shock from the Strait of Hormuz will ultimately be remembered as the moment India’s packaging industry found its domestic anchor in circularity.